For as long as I can remember, PF geeks/fans/experts have encouraged the use of a budget. In helping people understand how to create a budget, much of their advice directs folks to track their expenses (i.e. categorize and write down everything you spend) for a month, and then use such numbers as a basis for your budget (i.e. the month to month plan for spending your money). My major beef with this technique is that one month of expenses (and income) doesn't look like every other month of the year. Sure, I have

fixed expenses and

variable expenses to look forward to every month, but how do I accurately plan for the

miscellaneous expenses? And how do I remind myself of my progress (i.e. spending within my income and setting aside funds for goals)?

I track

ALL the time. Yup. That's what I do. Moreover, I take a summary of my expenses and average it with previous pay periods (that's how I break down my expense tracking; as per my regular paycheck). Next year, I look forward to tracking on a monthly basis. To give you an idea of how this budget/tracker tool works, I've included a

blank copy here. I encourage you to use it if 1) you're not currently tracking your expenses/budget or 2) what you're using isn't working for you. I'd love to hear your feedback. But before we get started, here are a few assumptions:

- You have a bank checking account that you regularly use for transactions.

- You have stable income (i.e. you know how much you get paid for each month)

Okay, here's your guide:

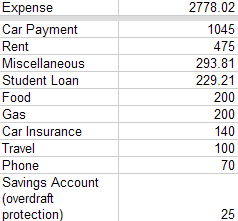

1st Tab, Annual Budget: In general, this is what your month-to-month expenses look like. Simply insert the monthly expense and the spreadsheet will calculate your annual expense for said category. Your total annual expense should be equal to or less than your regular annual income. For the folks who work on commission and have widely varying income, you could estimate the lower end of your anticipated income...or use a tool that's better suited for you.

2nd Tab, "Insert Month Here": This is where you will track your expenses. Feel free to change the name of the tab for the month that you will be tracking expenses. Enter your regular monthly income in cell M3 (it has a little orange ticker in the cell for a comment box). The reason this is here is so your expenses can be deducted from it to show you what you have available to spend. I often check this number against my bank statements. If you have additional income during a specific month, you can add it to your regular income; remember to add a note about the amount and source of those extra funds (ex: tax refund, $3269.11; overtime, $563.97).

For the "date" column, type in the date that you make a purchase (ex: 11/04). For the "Description" column, type in what you purchased and any details you'd like (ex: Publix (groceries), PetSmart (toys), TGIFs (+$10 tip). If you run out of space for the details you deem critical, simply "insert a comment" to add additional notes. Now, enter the amount that you spent at the respective store/on the respective item in the appropriate column. For example, if I spent $56.93 at Publix, I would enter that dollar amount in the food column. Likewise, if I spent $46.36 at TGIF, I would enter that dollar amount in the food column. Now, if I used my credit card to make a purchase at TGIF, I would not enter it into the food column, I'd enter the amount spent in the "CC Transactions" column. Similarly, if you use cash, track all of your cash transactions in the appropriate columns. If my categories of spending don't work for you, change them!

3rd Tab, Summary of Expenses: This is pretty straightforward. Enter the total spending per category per month in the appropriate line. Put another way, copy the amounts from row 4 of your "Month" sheet to the corresponding month in the summary sheet. This last sheet will average out what you spend per category of spending (ex. food, entertainment, bills, etc.). You can then compare these amounts to your annual budget to explore opportunities for improvement.

Since using this budget tracker - about 2 years, now - I've gained an incredible sense of control over my finances. I can project where I will pull money from to make up for other expenses, keep an eye on how much I'm spending, and remain mindful about credit card transactions. I hope it is equally helpful for you!

{kind=link}

{kind=link}

{kind=link}