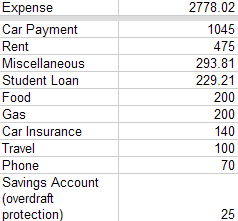

I can’t believe that I got so caught up on having a little bit of spending money that I completely neglected a time-sensitive goal. You see, when I revised my debt reduction plan so that I would pay off my car note by the end of February 2011, I figured I’d have $1245 for March and $350 for [the first half of] April 2011. My plan was to place this amount ($1595) into my Roth IRA. In a previous post, I listed maxing out my Roth IRA as a goal; by sticking to the “$1245/month” plan, I would be $2288.75 short of reaching this goal. (i.e. reaching $5,000; I've contributed $1,116.25, to date). Well, since I’ve updated my debt reduction plan (i.e. reduced my monthly car payments from $1245 to $1045) and paid off my credit card, now I won’t pay off my car until the beginning/middle of April 2011.

And the issue about my goal being time-sensitive? The IRS won’t allow me to make contributions to my Roth IRA for 2010 past April 15, 2011. Each year, I’m allowed to contribute a maximum of $5,000, and I would like very much to begin the trend of doing this sooner than later (I gotta have my money "in the game!"). Going forward, this will be a cinch, because I won’t have a car payment and credit card debt sabotaging my savings.

So, what should I do? Here are a few ideas that crossed my mind:

1) Contribute. Postpone my car payoff date and restore contributions to max out the Roth. If I did this from November 2010 through March 2011 (5 months), I would make my regular car payment ($269.11) and would contribute $776.75 to the Roth (5 months times $776.75 equals the $3,883.75 needed to reach $5K). Additionally, I’d be able to pay off the car loan by the end of October 2011 if, starting May 2011, I paid $729/month to the note (includes minimum payment).

And the issue about my goal being time-sensitive? The IRS won’t allow me to make contributions to my Roth IRA for 2010 past April 15, 2011. Each year, I’m allowed to contribute a maximum of $5,000, and I would like very much to begin the trend of doing this sooner than later (I gotta have my money "in the game!"). Going forward, this will be a cinch, because I won’t have a car payment and credit card debt sabotaging my savings.

So, what should I do? Here are a few ideas that crossed my mind:

1) Contribute. Postpone my car payoff date and restore contributions to max out the Roth. If I did this from November 2010 through March 2011 (5 months), I would make my regular car payment ($269.11) and would contribute $776.75 to the Roth (5 months times $776.75 equals the $3,883.75 needed to reach $5K). Additionally, I’d be able to pay off the car loan by the end of October 2011 if, starting May 2011, I paid $729/month to the note (includes minimum payment).

P.S. I'd max my 2011 Roth by saving $316/month from May 2011 to October 2011 ($1896), $535/month from November 2011 to March 2012 ($2,675) and including the $430 overpayment for the car note from October 2011.

2) Screw it. Get $625 per month ready for every month starting May 2011 in order to max out the account for 2011 and pay no additional interest on the car loan.

Update: I had my garage sale! Okay, so I probably shouldn't put an exclamation point after that statement, considering that my operation got shut down with a quickness (who knew I couldn't have a sale on the storage company's property? I knew I should have read the contract!) Nevertheless, I earned $93 for my goods and spent less than $50 renting a pick up truck to transport the "leftover" goods to a nearby Salvation Army. Hooray for $97/month restored to my budget!!!

{kind=link}

{kind=link}