Earlier this week, I shared my budget and categories of spending that were non-negotiable.

Today we will cover the part of my budget where I have a little flexibility: meet my “maybe negotiable” expenses.

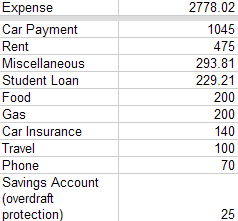

I spend $565 in “maybe negotiable” categories each month. Here they are:

Food, $200: While I’ve never been one to order out “every day of the week”, I do enjoy an occasional indulgence such as happy hour or a $7 slice of cake (Hey, don’t judge me! We both know that Cheesecake Factory has it going on!). I recently discovered that I could shave about $40 off of my food expenses if I remained diligent about packing my lunch and not eating out “so much” (ex. twice a week). When it comes to grocery shopping, I make a list based on what’s in the sale circular. I haven’t been a super-duper-coupon-clipping-lady when it comes to food shopping, so there might be an opportunity here. By the way, I can get down like Cookie Monster...

Gas, $200: Currently, carpooling and public transit are not feasible options for my day-to-day travel because: a) my job requires that I have my own transportation (luckily, I don’t have to travel out of the office everyday; but when I do, I am reimbursed for it), and b) although I live 40 miles away from the J-O-B, there is no direct route (via mass transit) from where I am to where I need to be. I’d have to drive at least three-quarters of the way or take fifty million transfers to get to work (okay, so 50,000,000 transfers is a bit of an exaggeration).

{kind=link}

Car Insurance: $140: I could pay the entire premium out of my savings (and eliminate the inconvenient “convenience fee” tacked on for monthly payments), break my premium into larger chunks (ex. pay it over the course of 2 or 3 months vs. monthly), or do what I’m doing (pay in monthly installments and spend $25 over the course of 5 months to pay the entire amount. I should mention that 1/6 of my car insurance premium is less than $140 I currently pay; at the rate I’m going, I’ll pay the entire premium in less than 6 months.

Savings Account, $25: Not too long ago, I was familiar with overdraft fees in a way that’s embarrassing to admit to. In order to mitigate this issue, I signed up for overdraft protection with my primary bank. To avoid monthly maintenance fees on the savings account where the overdraft service pulls from, I have to maintain a monthly deposit of at least $25. Staying on top of my account balances and outstanding transactions has resulted in ZERO overdraft fees for me (YAY!). In fact, the last time I incurred such a fee was April 2009 ($245 of overdraft fees in that month alone; you better believe that I signed up for overdraft protection the following month. I was absolutely disgusted by my waste and irresponsibility!)

{kind=link}

No comments:

Post a Comment