...and I'm back! I sincerely apologize for being absent last week, but I'm back now =)

So, what's been going on? The usual, the not-so-usual and some more of the usual. Let's get started with the usual.

The Usual

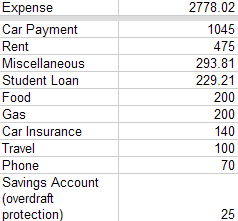

I've been diligently tracking my

expenses in my tracker housed on Google Docs. I've exceeded my allocated amount for food and car expenses: footing the bill for my sister's birthday dinner; being a bit impulsive (eating out, mostly); increasing gas prices (is anyone else paying around $3/gallon?); and regular car maintenance (the coupon for my oil change this time around wasn't $19.99 + tax :<).

The Unusual

Holiday stuff. You know, buying gifts and bringing in whatever you signed up for for the holiday party at work. Actually, the work stuff was easy. We had a cookie swap and I brought a non-cookie item to swap: brownies. Had I not been distracted by the massive amounts of sugar tempting my waistline, I would've repackaged the cookies and sold them for income =) The not so easy stuff is holiday shopping. To cover the expense of Christmas gifts without regretting it in January (i.e. financing all purchases with my credit card with no clear way of paying it off), I decided to decrease the amount of my car payment this month to $356.98 (I know, it's a weird amount). At any rate, doing so allowed me to spend $705 of "car payment" money on gifts for my parents, sisters, boyfriend, best friend and godson. Sadly, I've spent $690 and some change and I still have a few items to pick up. Fortunately, I have a few bucks in my "immediate access" savings account (this is NOT my emergency savings account) that I'm comfortable using to cover these items.

More of the Usual

Revisiting goals and planning. I spent quite a bit of time today updating my savings plan [another Google spreadsheet I use to track the balances of my savings account linked to my checking account (see "immediate access" savings account above), my ING Direct account (emergency savings), my Roth IRA, regular brokerage account and 403(b)] and reconciling it with my 2011 budget. It feels SO DARN GOOD to account for every single penny. Did you get that? EVERY. SINGLE. PENNY. I know where it came from or where it went and for what purpose. Moments like these help me feel in control of my finances, and not vice versa...

something that I occasionally freak out about. Nevertheless, I am on track to enjoy my boyfriend's birthday (I've planned a surprise trip for him), my girlfriend's birthday (we're going to be "Bahama Mamas"), a winter weekend getaway in the Poconos with a gaggle of friends, my 2nd year anniversary with the beau, paying off my car note, and my friend's wedding. And all of these things are happening in the first half of the year! To be fair, I am making assumptions about my anticipated tax refund, the bulk of which will go towards principal reduction on the note. Everything else is accounted for (i.e. planned to come from my regular income).

As I prepare for 2011 (and the end of my car note, hooray!), I'm considering the opportunities to save more, invest more, and to be better equipped to pay for travel and entertainment expenses that inevitably have a habit of "popping up." My post later this week will focus on financial goals [and concomitant action plans] for 2011.

How have you been handling expenses related to the holiday season? Did you set up a budget? Are you "winging it?" Have you started to plan for 2011 financially? Have/will you do a "2010 Year in Review" for your finances?

{kind=link}

{kind=link}