I'll keep it short today. Here are a few updates:

Keep the Change

At the beginning of the month, I enrolled in BofA's "Keep the Change" program. To date, I've "kept" $17.98 in change. For the first three months of the program, the bank will match my savings, penny-for-penny. This (i.e. the match) sure beats the heck out of their sorry interest rate.

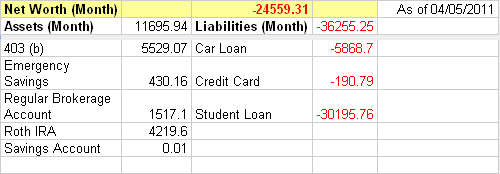

Credit Card

Four billing cycles for 2011 have passed and I am still not paying interest on my credit card. Woohoo for "free credit". However, I should keep a closer eye on what balance I carry at any time. You've probably heard that if you carry a balance that you should keep it under 30% of what's available to you (if you haven't heard this, you just did.....you can thank me later ;>....and if you don't believe me, look what Kiplinger's said here). Although I do not carry over a balance (from billing cycle to billing cycle), I am also unaware of when my credit card company reports such information to the credit reporting bureaus. As such, I prefer to stay on the side of caution.

Car Stuff

My balance is just over $5,000 and if I stay on track (and not go crazy shopping for two upcoming weddings and go bezerks with graduation gifts) then I'll pay the note off by the end of August. What's more 'exciting' is that I haven't been made aware of any repairs needed for my car. We know how repairs derail the car note elimination plan.